Authored by the expert who managed and guided the team behind the South Africa Property Pack

Everything you need to know before buying real estate is included in our South Africa Property Pack

If you are a foreigner thinking about buying property in South Africa, you will need to budget for more than just the purchase price because closing costs, taxes, and professional fees can add a significant amount to your total spending.

This guide breaks down every cost you can expect when buying residential property in South Africa in 2026, from transfer duty and conveyancing fees to hidden surprises like municipal clearance charges.

We constantly update this blog post to reflect the latest rates and regulations so you always have fresh, reliable information.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in South Africa.

Overall, how much extra should I budget on top of the purchase price in South Africa in 2026?

How much are total buyer closing costs in South Africa in 2026?

As of early 2026, total buyer closing costs in South Africa typically range from 6% to 12% of the purchase price, which means on a R2,000,000 home (around USD 108,000 or EUR 100,000), you should budget roughly R120,000 to R240,000 (USD 6,500 to USD 13,000 or EUR 6,000 to EUR 12,000) on top of what you pay for the property itself.

The minimum extra budget possible for closing costs in South Africa is around 2% to 3% of the purchase price (about R24,000 to R36,000, or USD 1,300 to USD 1,950, or EUR 1,200 to EUR 1,800 on a R1,200,000 property), but this only applies if you buy below the transfer duty threshold of R1,210,000 and pay cash without a mortgage.

The maximum extra budget buyers should realistically plan for closing costs in South Africa is around 12% to 15% of the purchase price (for example, R300,000 to R375,000 on a R2,500,000 home, or USD 16,200 to USD 20,300, or EUR 15,000 to EUR 18,750), especially if you are financing the purchase with a bond and buying an expensive property where transfer duty climbs steeply.

The main factors that determine whether your closing costs fall at the low end or high end in South Africa are the purchase price (which affects your transfer duty bracket), whether you need a mortgage (which adds bond registration fees), and how complex the transaction is (for example, buying in a sectional title scheme with levies and clearance requirements or sending funds from abroad with exchange control procedures).

What's the usual total % of fees and taxes over the purchase price in South Africa?

The usual total percentage of fees and taxes over the purchase price in South Africa is around 6% to 10% for most residential transactions, though this varies significantly depending on the property value and whether you are taking out a mortgage.

The realistic low-to-high percentage range that covers most standard property transactions in South Africa is 2% to 4% for properties under R1,210,000 (where transfer duty is zero), 6% to 9% for mid-range properties between R1,500,000 and R3,000,000, and 8% to 12% for high-value properties worth several million rand.

Of that total percentage, government taxes (primarily transfer duty) typically account for the largest portion on properties above R1,210,000, while professional service fees (conveyancing attorneys, bond attorneys, and Deeds Office charges) make up a smaller but still significant share, usually around 2% to 4% combined.

By the way, you will find much more detailed data in our property pack covering the real estate market in South Africa.

What costs are always mandatory when buying in South Africa in 2026?

As of early 2026, the mandatory costs when buying property in South Africa include transfer duty (or VAT if buying from a VAT-registered developer), conveyancing attorney fees plus 15% VAT, Deeds Office transfer fees, and if you are financing the purchase, bond registration attorney fees plus VAT and Deeds Office bond fees.

Optional but highly recommended costs for buyers in South Africa include a professional building inspection (especially for older homes), an independent property valuation, and a few hours of tax advisor time if you plan to rent out the property or are buying as a non-resident who may face withholding tax obligations when selling later.

Don't lose money on your property in South Africa

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What taxes do I pay when buying a property in South Africa in 2026?

What is the property transfer tax rate in South Africa in 2026?

As of early 2026, the property transfer tax in South Africa (called transfer duty) is charged on a sliding scale starting at 0% for properties up to R1,210,000, then rising through brackets of 3%, 6%, 8%, 11%, and reaching a maximum marginal rate of 13% for the portion of the value above R11,000,000.

There are no extra transfer taxes for foreigners buying property in South Africa because the transfer duty brackets apply equally to South African citizens and foreign buyers, meaning your nationality does not increase the tax you pay on the purchase.

Buyers pay VAT instead of transfer duty on residential property purchases in South Africa only when buying from a VAT-registered vendor (typically a property developer) who is selling in the course of their business, and in that case the 15% VAT is usually included in the advertised price, though you should always confirm whether the quoted price is VAT-inclusive.

In South Africa, there is no separate stamp duty line item like in some other countries because transfer duty is the main transaction tax for residential property transfers, and your conveyancing attorney handles the calculation and payment to SARS as part of the transfer process.

Are there tax exemptions or reduced rates for first-time buyers in South Africa?

South Africa does not offer a specific first-time buyer tax exemption or reduced rate, but all buyers benefit from the 0% transfer duty threshold on properties up to R1,210,000, which in practice helps first-time buyers purchasing entry-level homes the most.

If you buy property through a company instead of as an individual in South Africa, the transfer duty rules still apply at purchase, but the bigger tax differences show up later in how rental income, capital gains, and estate planning are treated, so buying via a company is more of a long-term tax planning decision than a way to save on closing costs.

There is a tax difference between buying a new-build property versus a resale property in South Africa because new-builds from VAT-registered developers may include 15% VAT in the price instead of transfer duty, so you need to confirm in your offer to purchase whether the price is VAT-inclusive and whether transfer duty applies.

Since South Africa does not have a formal first-time buyer exemption with special documentation requirements, the main condition to benefit from the 0% threshold is simply that the property price must be R1,210,000 or below, which your conveyancing attorney will verify as part of the standard transfer process.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in South Africa versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

Which professional fees will I pay as a buyer in South Africa in 2026?

How much does a notary or conveyancing lawyer cost in South Africa in 2026?

As of early 2026, conveyancing attorney (transfer attorney) fees in South Africa typically range from 0.5% to 1.3% of the purchase price before VAT, so on a R2,000,000 property, you would pay roughly R10,000 to R26,000 (USD 540 to USD 1,400 or EUR 500 to EUR 1,300) in legal fees, plus another 15% VAT on top of that.

Conveyancing fees in South Africa are typically charged as a percentage of the property price following the LSSA guideline tariff, though the actual fee is negotiable and varies slightly between law firms.

Translation or interpreter services for foreign buyers in South Africa cost approximately R250 to R600 per page (USD 14 to USD 32 or EUR 13 to EUR 30) for certified sworn translations of identity documents and affidavits, while live interpretation at a signing appointment might cost R1,500 to R5,000 (USD 80 to USD 270 or EUR 75 to EUR 250) depending on duration and travel.

If you plan to rent out your South African property or are a non-resident who may face withholding tax when selling, hiring a tax advisor for one or two hours of consultation is worth the cost, which typically ranges from R1,500 to R4,000 (USD 80 to USD 215 or EUR 75 to EUR 200) and can save you from expensive compliance mistakes later.

We have a whole part dedicated to these topics in our our real estate pack about South Africa.

What's the typical real estate agent fee in South Africa in 2026?

As of early 2026, the typical real estate agent fee in South Africa is in the mid single-digit percentages of the sale price (commonly around 5% to 7.5%), plus 15% VAT if the agency is VAT-registered, though this commission is negotiated between the seller and the agent rather than set by law.

In South Africa, the seller pays the agent fee in most transactions, so as a buyer you typically do not write a separate cheque for commission, although the commission does indirectly affect the price since it comes out of what the seller nets from the sale.

The realistic low-to-high range for agent fees in South Africa runs from around 4% on the low end (often for very high-value properties where agents compete for listings) to 7.5% or higher on the high end (more common for standard residential sales), and you should always clarify with the seller or agent who is responsible for paying this cost.

How much do legal checks cost (title, liens, permits) in South Africa?

Legal checks including title searches, liens verification, and permit reviews in South Africa are usually bundled into your conveyancing attorney's disbursements and typically add R500 to R2,000 (USD 27 to USD 108 or EUR 25 to EUR 100) in small line items for deeds searches, FICA compliance, and administrative costs.

A property valuation fee in South Africa typically costs R1,500 to R4,000 (USD 80 to USD 215 or EUR 75 to EUR 200) depending on the property location and complexity, and your bank will usually require one if you are financing the purchase, though cash buyers can also commission one for peace of mind.

The most critical legal check that should never be skipped in South Africa is the title deeds search and verification performed by your conveyancing attorney, as this confirms the seller actually owns the property, reveals any existing bonds or servitudes, and ensures you can receive clear title.

Buying a property with hidden issues is something we mention in our list of risks and pitfalls people face when buying real estate in South Africa.

Get the full checklist for your due diligence in South Africa

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What hidden or surprise costs should I watch for in South Africa right now?

What are the most common unexpected fees buyers discover in South Africa?

The most common unexpected fees buyers discover in South Africa include municipal clearance delays that cause knock-on costs (extra rent, storage, foreign exchange timing), sectional title scheme charges like levy clearances and moving deposits, small attorney disbursements that add up (couriers, deeds searches, FICA admin), and bank or foreign exchange fees when transferring funds from abroad through authorised dealers.

Yes, there can be unpaid property taxes or municipal debts you could inherit when purchasing in South Africa, which is exactly why the clearance certificate process exists to block transfers until the seller's municipal accounts are settled, though you should still ensure your conveyancer verifies all outstanding balances before registration.

Buyers do get scammed with fake listings or fake fees in South Africa, most commonly through fake deposit requests to fraudulent bank accounts, impersonation of estate agents or conveyancers, and doctored invoices, so you should only pay large transaction amounts into your conveyancing attorney's trust account after independently verifying the banking details by calling a known number rather than relying on email signatures.

Fees that are usually not disclosed upfront by sellers or agents in South Africa include small conveyancing disbursements (postage, searches, e-filing fees) that appear later on the attorney's statement, bank receiving fees for international transfers, and pro-rata levies or municipal charges that only become clear once the clearance process begins.

In our property pack covering the property buying process in South Africa, we go into details so you can avoid these pitfalls.

Are there extra fees if the property has a tenant in South Africa?

Extra fees when buying a property with a tenant in South Africa may include lease documentation and cession administration costs (typically R500 to R2,000 or USD 27 to USD 108 or EUR 25 to EUR 100), deposit handover verification, and potential onboarding fees if you inherit an existing property management company.

When purchasing a tenanted property in South Africa, the buyer inherits the existing lease agreement and must honour its terms until expiry, which means you take over as landlord with all the rights and obligations that come with the current rental contract.

It is generally not possible to terminate the existing lease immediately after purchase in South Africa unless the lease contains a specific clause allowing this, because the tenant's rights transfer with the property and you must wait until the lease ends or follow proper legal termination procedures.

A sitting tenant in South Africa can affect the property's market value either positively (as a guaranteed income stream for investors) or negatively (if the lease terms are unfavourable or the buyer wants vacant occupation), and sellers often discount tenanted properties by 5% to 10% when marketing to owner-occupier buyers.

If you want to optimize your rental strategy, you can read our complete guide on how to buy and rent out in South Africa.

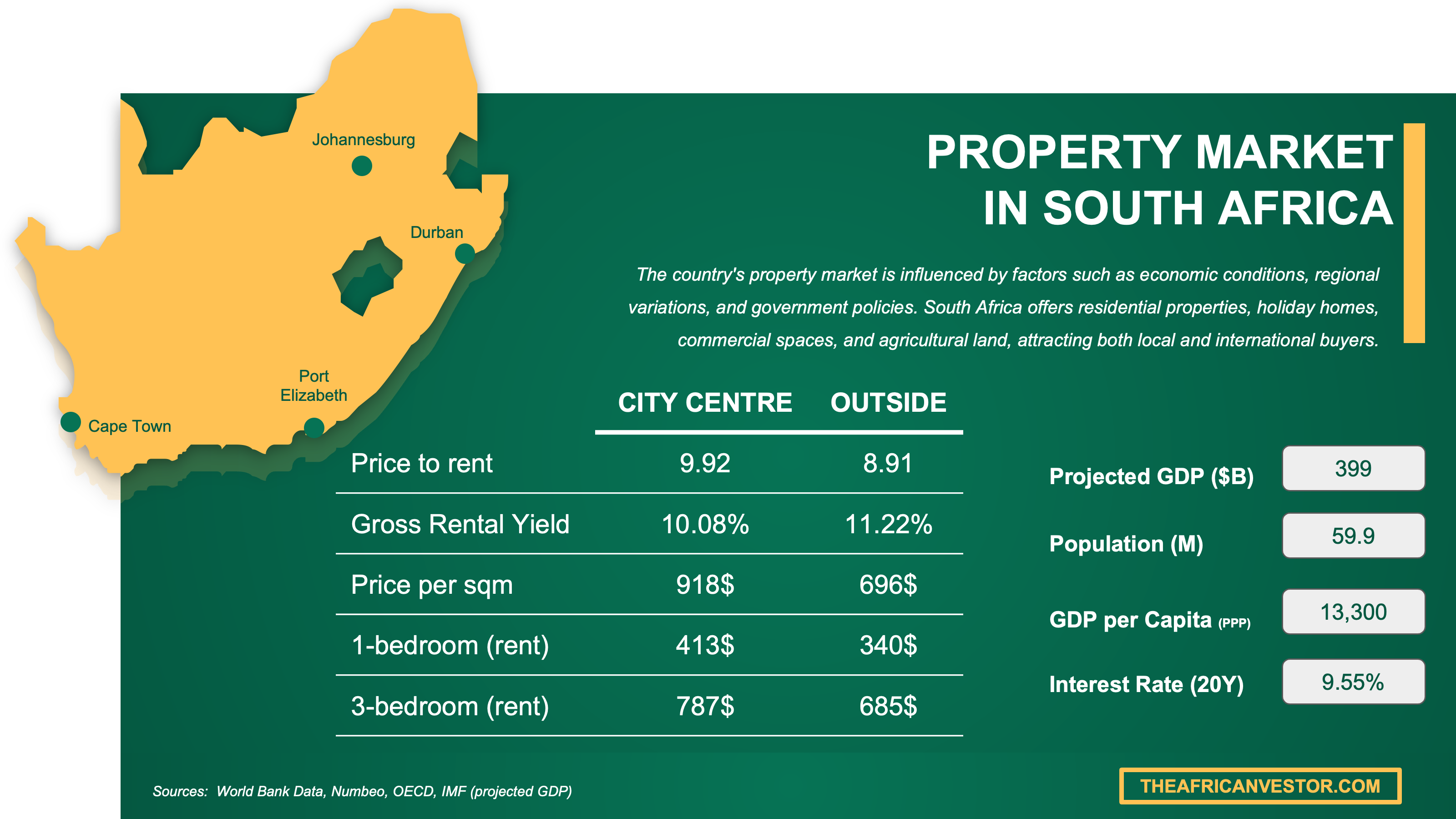

We have made this infographic to give you a quick and clear snapshot of the property market in South Africa. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which fees are negotiable, and who really pays what in South Africa?

Which closing costs are negotiable in South Africa right now?

Negotiable closing costs in South Africa include conveyancing attorney professional fees (though many start from the LSSA guideline tariff), bond registration attorney fees, and in some cases bank arrangement fees or valuation fees if you negotiate with your lender.

Closing costs that are fixed by law or regulation and cannot be negotiated in South Africa include the transfer duty brackets set by SARS and the Deeds Office registration fees published in the official schedule, as these are government-mandated charges that apply equally to everyone.

Typical discounts buyers can realistically achieve on negotiable fees in South Africa range from 10% to 20% off the attorney's professional fee quote, especially if you are a repeat client, are referred by the estate agent, or are handling a straightforward transaction with a clear title.

Can I ask the seller to cover some closing costs in South Africa?

You can always ask the seller to cover some closing costs in South Africa, but the common market practice is for the buyer to pay transfer-related costs and the seller to pay agent commission, so sellers agreeing to cover buyer costs is relatively uncommon except in slow markets or when a property has been listed for a long time.

The specific closing costs sellers are most commonly willing to cover in South Africa are minor items like clearance certificate admin fees or small municipal balance top-ups, rather than major expenses like transfer duty or conveyancing fees which are traditionally the buyer's responsibility.

Sellers are more likely to accept covering closing costs in South Africa when the property market is slow (a buyer's market), when the property has been on the market for several months without offers, or when the buyer is offering a quick close with cash rather than waiting for bond approval.

Is price bargaining common in South Africa in 2026?

As of early 2026, price bargaining is common and expected in South Africa, with buyers and sellers typically negotiating rather than accepting the first asking price, especially in cities like Cape Town (Sea Point, Green Point, Gardens), Johannesburg (Sandton, Rosebank, Melrose), and Durban (Umhlanga, Morningside).

Buyers in South Africa typically negotiate 3% to 10% below the asking price, which translates to R45,000 to R150,000 off a R1,500,000 property (USD 2,400 to USD 8,100 or EUR 2,250 to EUR 7,500), with the lower end applying to well-priced listings in hot suburbs and the higher end applying to stale listings or properties needing renovation.

Don't sign a document you don't understand in South Africa

Buying a property over there? We have reviewed all the documents you need to know. Stay out of trouble - grab our comprehensive guide.

What monthly, quarterly or annual costs will I pay as an owner in South Africa?

What's the realistic monthly owner budget in South Africa right now?

A realistic monthly owner budget in South Africa (excluding mortgage payments) is around R2,500 to R8,000 per month (USD 135 to USD 430 or EUR 125 to EUR 400) for a standard residential property, depending on the municipality, property size, and whether you live in a sectional title scheme with levies.

The main recurring expense categories that make up this monthly budget in South Africa are municipal property rates (your annual property tax paid monthly), municipal services (water, electricity, refuse removal), and if applicable, body corporate or homeowners association levies for security and maintenance of common areas.

The realistic low-to-high range for monthly owner costs in South Africa is R1,500 to R4,000 (USD 80 to USD 215 or EUR 75 to EUR 200) for a freestanding house without levies in a smaller municipality, up to R6,000 to R15,000 (USD 325 to USD 810 or EUR 300 to EUR 750) for a large property in a premium security estate in major cities like Cape Town or Johannesburg.

The monthly cost that tends to vary the most in South Africa is body corporate levies, which can range from R1,000 to over R5,000 per month depending on the amenities (pools, gyms, 24-hour security) and the size and age of the complex.

You can see how this budget affect your gross and rental yields in South Africa here.

What is the annual property tax amount in South Africa in 2026?

As of early 2026, annual property tax (called municipal rates) in South Africa typically amounts to 0.5% to 1.2% of the municipal valuation per year, so on a property valued at R2,000,000, you would pay roughly R10,000 to R24,000 per year (USD 540 to USD 1,300 or EUR 500 to EUR 1,200) before any rebates.

The realistic low-to-high range for annual property taxes in South Africa is R5,000 to R15,000 (USD 270 to USD 810 or EUR 250 to EUR 750) for properties valued around R1,500,000, up to R30,000 to R60,000 (USD 1,620 to USD 3,240 or EUR 1,500 to EUR 3,000) for high-value properties worth R5,000,000 or more, with significant variation between municipalities.

Property tax in South Africa is calculated by applying a cent-in-the-rand rate (set by each municipality) to the municipal valuation of your property, meaning the same property would attract different rates depending on whether it is in Cape Town, Johannesburg, Durban, or a smaller town.

Some exemptions or reductions are available for certain property owners in South Africa, including rebates for pensioners, disabled persons, and indigent households, though eligibility and amounts vary by municipality and you need to apply directly to your local council.

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of South Africa. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

If I rent it out, what extra taxes and fees apply in South Africa in 2026?

What tax rate applies to rental income in South Africa in 2026?

As of early 2026, rental income in South Africa is taxed at your marginal income tax rate as an individual, which means rates range from 18% for the lowest bracket up to 45% for taxable income exceeding R1,817,000 per year.

Yes, landlords in South Africa can deduct legitimate expenses from rental income before calculating tax, including property maintenance, insurance, municipal rates, agent management fees, interest on a bond used to buy the property, and certain repairs, though the deductibility of some items (like mixed-use expenses) can be complex.

The realistic effective tax rate range after deductions for typical landlords in South Africa is around 10% to 30% of net rental profit, depending on your total taxable income, how many deductible expenses you have, and your marginal tax bracket.

Foreign property owners in South Africa pay the same rental income tax rates as residents on their South African-sourced rental income, but they should be aware of potential double taxation issues with their home country and may need to claim relief under an applicable tax treaty.

Do I pay tax on short-term rentals in South Africa in 2026?

As of early 2026, short-term rental income in South Africa (such as Airbnb income) is taxable as ordinary income, meaning you must declare it and pay tax at your marginal rate just like long-term rental income.

Short-term rental income is generally taxed the same as long-term rental income in South Africa under income tax rules, but there is an important VAT consideration: if your short-term rental activity qualifies as "commercial accommodation" and exceeds the VAT registration threshold, you may need to register for VAT and charge 15% on your rental income, which is a complexity that rarely applies to long-term residential letting.

If you want to optimize your rental strategy, you can read our complete guide on how to buy and rent out in South Africa.

Get to know the market before buying a property in South Africa

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

If I sell later, what taxes and fees will I pay in South Africa in 2026?

What's the total cost of selling as a % of price in South Africa in 2026?

As of early 2026, the total cost of selling a property in South Africa typically ranges from 6% to 10% of the sale price, covering agent commission, compliance certificates, legal fees, and potential capital gains tax.

The realistic low-to-high percentage range for total selling costs in South Africa is 5% to 7% if you have no taxable capital gain and negotiate a competitive agent commission, up to 12% to 15% if you have a large capital gain, need expensive compliance fixes, and pay standard commission rates.

The specific cost categories that typically make up total selling costs in South Africa include estate agent commission (usually the largest item at 5% to 7.5% plus VAT), compliance certificates (electrical, gas, beetle, plumbing where applicable), bond cancellation attorney fees if you have a mortgage, and capital gains tax on any profit.

The single cost that is usually the largest contributor to selling expenses in South Africa is the estate agent commission, which at 5% to 7.5% of the sale price plus 15% VAT can easily exceed R100,000 on a R2,000,000 sale.

What capital gains tax applies when selling in South Africa in 2026?

As of early 2026, capital gains tax in South Africa for individuals works by including 40% of your capital gain in your taxable income and taxing it at your marginal rate, which means the maximum effective CGT rate is 18% of the gain (40% inclusion x 45% top marginal rate).

Exemptions to capital gains tax available in South Africa include a primary residence exclusion (up to R2,000,000 of gain is exempt if you lived in the property as your main home), an annual exclusion of R40,000, and a R300,000 exclusion on death, so many homeowners selling their primary residence pay little or no CGT.

Foreigners do not pay a higher capital gains tax rate than residents when selling property in South Africa, but there is a significant procedural difference: when a non-resident sells, the buyer must withhold a portion of the purchase price (5% for individuals on properties over R2,000,000) and pay it to SARS as an advance against the seller's potential CGT liability.

Capital gain in South Africa is calculated by taking the sale price minus the base cost (original purchase price plus qualifying costs like transfer duty, improvements, and selling expenses), and you can also adjust the base cost upward using a time-apportionment method for properties held since before 1 October 2001.

We made this infographic to show you how property prices in South Africa compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about South Africa, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why it's authoritative | How we used it |

|---|---|---|

| SARS Transfer Duty Rates | SARS is the official South African tax authority that publishes legally binding tax brackets. | We used it as the primary source for 2026 transfer duty thresholds and marginal rates. We converted those brackets into practical budget ranges at common purchase prices. |

| SARS Transfer Duty Guide (TD01) | This is SARS's detailed interpretation guide explaining how transfer duty works. | We used it to confirm when transfer duty applies and who pays it. We cross-checked those rules against VAT guidance to clarify the interplay. |

| SARS VAT Overview | This is SARS's official page confirming the current VAT rate in South Africa. | We used it to anchor the 15% VAT rate applied to professional fees. We also clarified when VAT applies to property transactions. |

| SARS Individual Tax Rates | SARS publishes the official marginal tax brackets for individuals in South Africa. | We used it to explain how rental income is taxed at marginal rates. We also used it to compute the maximum effective capital gains tax rate. |

| SARS Capital Gains Tax Page | SARS is the source of truth for CGT inclusion rates and exclusions. | We used it to explain how CGT is calculated using inclusion rates. We then translated that into effective percentage ranges for budgeting. |

| SARS Non-Resident Withholding Guide | This is official SARS guidance on withholding when non-residents sell property. | We used it to warn foreign buyers about the withholding mechanism when they later sell. We explained that withholding is an advance collection, not an extra tax. |

| LSSA Conveyancing Fee Guidelines | The Law Society publishes the standard market benchmark for conveyancing fees. | We used it to estimate transfer and bond registration attorney fees by price. We then added VAT to give realistic cash-to-close budgets. |

| Deeds Office Fee Schedule | This is the official government fee schedule for registering property transfers. | We used it to price the mandatory Deeds Office charges in transfer and bond registration. We separated these government fees from negotiable lawyer fees. |

| City of Cape Town Property Rates | This official city budget document shows actual rate-in-the-rand charges. | We used it as a concrete example to estimate annual property rates in a major market. We then generalised to a South Africa-wide budgeting range. |

Get fresh and reliable information about the market in South Africa

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.