Authored by the expert who managed and guided the team behind the South Africa Property Pack

Everything you need to know before buying real estate is included in our South Africa Property Pack

South Africa is one of the few African countries where foreigners can buy and truly own residential property in their own name, including the land underneath it.

In this guide, we break down the legal rules, visa requirements, mortgage options, taxes, and step-by-step buying process that foreign buyers face in South Africa as of January 2026.

We update this article regularly to keep the information current and useful for your property search.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in South Africa.

Insights

- Foreigners in South Africa can legally purchase freehold houses, apartments, and land in their own name, with ownership registered through the Deeds Office, which is rare on the African continent.

- Non-resident buyers in South Africa typically face a maximum loan-to-value ratio of around 50%, meaning you should prepare a deposit of at least half the property price.

- As of January 2026, the prime lending rate in South Africa sits at 10.25%, so foreign buyers can expect mortgage rates between 10.25% and 12.25% depending on their profile.

- Buying property in South Africa does not grant residency or citizenship, so if you want to live there long-term, you will need to apply through work, business, retirement, or family pathways.

- The SARS withholding mechanism can trap non-resident sellers: if you do not file the right paperwork early, up to 10% of your sale proceeds may be withheld by the buyer on behalf of the tax authority.

- Total closing costs for cash buyers in South Africa typically range from 4% to 6% of the purchase price, rising to 6% to 9% if you finance with a mortgage bond.

- Transfer duty in South Africa is progressive and starts at 0% for properties under 1.1 million rand, so entry-level buyers benefit from significant savings.

- Municipal property rates in South Africa vary widely by city and can range from roughly 0.6% to 1.2% of the municipal valuation per year.

- South Africa taxes non-resident owners on rental income earned from South African property, so you will need to register with SARS and file annual returns.

What can I legally buy and truly own as a foreigner in South Africa?

What property types can foreigners legally buy in South Africa right now?

As of January 2026, foreigners can legally buy the same mainstream residential property types as South Africans, including freehold houses, sectional title apartments, townhouses, cluster homes, and homes in security estates.

The most important legal condition is that the transaction must be properly registered through the Deeds Office, and you must comply with banking identity rules and exchange control requirements for moving money into and out of South Africa.

Beyond the registration requirement, sectional title properties like apartments and townhouses often come with body corporate rules that can restrict things like pets, renovations, short-term rentals, and minimum lease periods.

For vacant residential land, foreigners can also purchase and own plots to build on, though these carry higher risk because development timelines and municipal approvals can be unpredictable.

Finally, please note that our pack about the property market in South Africa is specifically tailored to foreigners.

Can I own land in my own name in South Africa right now?

Yes, most foreigners can own land in their own name in South Africa when they buy a freehold house or a vacant residential plot, because freehold ownership includes the land (called an "erf") and is registered directly in your name at the Deeds Office.

This applies to virtually all types of residential land, though the practical challenges are not about whether you may own it, but rather about how you fund the purchase and how you later repatriate sale proceeds when you sell.

To make future repatriation easier, you should keep a clear paper trail showing that the original purchase funds came from abroad, which makes it simpler for banks and exchange control processes to approve the outflow.

By the way, we cover everything there is to know about the land buying process in South Africa here.

As of 2026, what other key foreign-ownership rules or limits should I know in South Africa?

As of January 2026, the rules that most often affect foreign purchases in South Africa are not really about ownership restrictions, but about sectional title conduct rules, municipal zoning compliance, and the tax mechanics that apply when you sell as a non-resident.

South Africa does not have a foreign-ownership quota rule for apartments or condos like some Asian countries do, so you can buy into any building without worrying about hitting a percentage cap.

However, conveyancers and banks will require FICA compliance documentation (passport, proof of address, source of funds), and you may need to obtain a South African tax number if you plan to earn rental income or eventually sell the property.

There is no major regulatory change around foreign ownership expected in 2026, though the government periodically discusses land reform, and it is always wise to stay updated on any policy shifts that could affect property rights.

If you're interested, we go much more into details about the foreign ownership rights in South Africa here.

What's the biggest ownership mistake foreigners make in South Africa right now?

The single biggest ownership mistake foreigners make in South Africa is confusing "I signed the offer" with "I own the property," when in reality, ownership only becomes legal once the property is registered in the Deeds Office.

If a buyer assumes ownership before registration is complete, they might start renovations, move belongings in, or make financial commitments before the deal is actually finalized, which can lead to serious problems if the transfer falls through.

Other classic pitfalls in South Africa include relying solely on an estate agent without hiring a conveyancer for proper legal checks, buying a property with illegal building additions that become your problem, and failing to prepare for the SARS withholding mechanism that can hold back part of your proceeds when you sell as a non-resident.

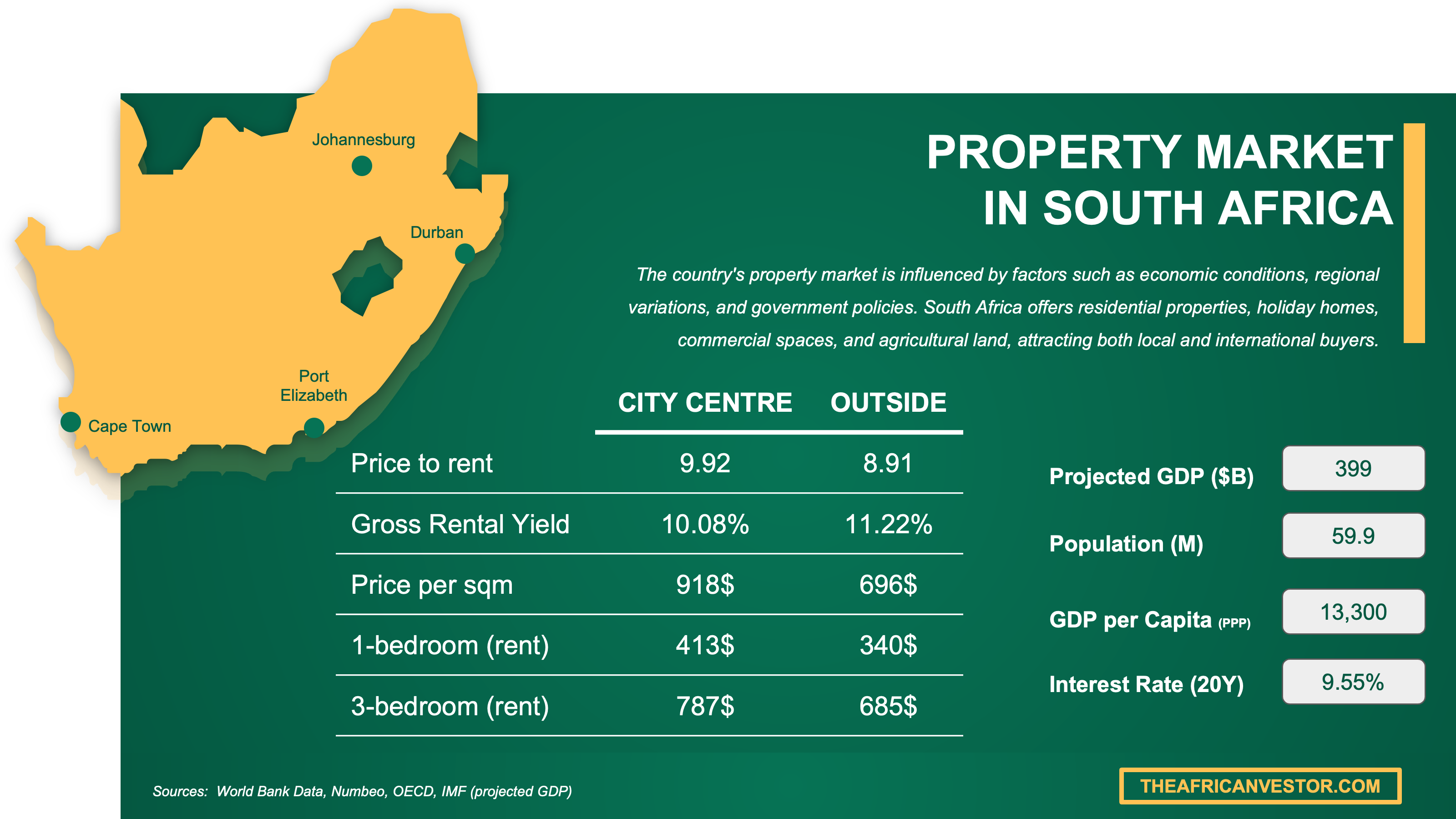

We have made this infographic to give you a quick and clear snapshot of the property market in South Africa. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which visa or residency status changes what I can do in South Africa?

Do I need a specific visa to buy property in South Africa right now?

You generally do not need a specific visa to buy property in South Africa, and yes, you can typically buy while on a tourist visa because purchasing property is a civil transaction, not a work right.

The most common administrative requirement that can slow down buyers without local residency is the FICA compliance process, where banks, conveyancers, and agents must verify your identity, address, and source of funds before the transaction can proceed.

While a South African tax number is not always required on day one, conveyancers frequently ask for one if you will earn rental income or eventually need SARS processes when you sell, so getting it early reduces friction.

A typical document set for a foreign buyer includes a valid passport, proof of your home address (like a utility bill), bank statements showing source of funds, and sometimes a letter from your foreign bank confirming the origin of the purchase money.

Does buying property help me get residency and citizenship in South Africa in 2026?

As of January 2026, buying residential property in South Africa does not, by itself, give you residency or citizenship, so if you want to live there long-term, you will need to apply through other established pathways.

South Africa does not have a "golden visa" or investor visa program that grants residency simply for purchasing real estate, unlike some other countries.

The standard routes to permanent residence in South Africa include work permits, business visas, retirement permits, financially independent permits, and family reunification, and each has its own eligibility criteria and minimum thresholds that do not depend on property ownership.

We give you all the details you need about the different pathways to get residency and citizenship in South Africa here.

Can I legally rent out property on my visa in South Africa right now?

Your visa status in South Africa generally does not restrict your ability to own and rent out your property, and many foreign owners manage their rentals from abroad through local letting agents.

You do not need to live in South Africa to rent out your property, though you should be aware that rental income from a South African property is considered South African-source income and is taxable by SARS even if you are a non-resident.

Other important details include that some sectional title buildings and security estates have conduct rules that restrict short-term rentals or require minimum lease periods, so you should check the body corporate rules before buying if rental income is part of your plan.

We cover everything there is to know about buying and renting out in South Africa here.

Get fresh and reliable information about the market in South Africa

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

How does the buying process actually work step-by-step in South Africa?

What are the exact steps to buy property in South Africa right now?

The standard sequence to buy property in South Africa is: choose a property and do initial compliance checks, sign an Offer to Purchase with conditions, submit your FICA documents, apply for financing if needed, let the seller's conveyancer handle the legal transfer work, pay your buyer costs (transfer duty, conveyancing fees, deeds office fees), and finally wait for registration at the Deeds Office, which is when you become the legal owner.

You do not always need to be physically present for every step in South Africa, because many signatures can be handled via a power of attorney or through embassy and notary processes abroad, though your conveyancer will tell you which documents must be original or wet-signed.

The step that makes the deal legally binding for both buyer and seller is typically the signing of the Offer to Purchase once all suspensive conditions (like bond approval or inspections) have been fulfilled or waived.

From accepted offer to final registration at the Deeds Office, the typical timeline in South Africa is around 8 to 12 weeks, though this can vary depending on bond approvals, municipal clearances, and how quickly all parties provide documents.

We have a document entirely dedicated to the whole buying process our pack about properties in South Africa.

Is it mandatory to get a lawyer or a notary to buy a property in South Africa right now?

A conveyancing attorney is effectively mandatory in South Africa because property transfers must be prepared and lodged for registration at the Deeds Office, and only qualified conveyancers can do this work.

The key difference in South Africa is that conveyancers handle the transfer and registration process (preparing deeds, obtaining clearances, paying duties), while a separate attorney could be hired to review the Offer to Purchase contract and advise on your legal rights, though this is optional.

One key item that should be explicitly included in your conveyancer engagement is confirming that they will obtain all necessary clearances, including municipal rates clearance and body corporate levy clearance for sectional title properties, before registration.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in South Africa versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What checks should I run so I don't buy a problem property in South Africa?

How do I verify title and ownership history in South Africa right now?

The official registry you should use to verify title and ownership history in South Africa is the Deeds Office, where your conveyancer can run a deeds search to confirm the current registered owner and the exact property description (erf number or sectional title unit).

The key title document you should request is the title deed itself, which shows the registered owner's name, the property description, and any conditions or servitudes attached to the land.

A realistic look-back period for ownership history checks in South Africa is typically 10 to 20 years, which allows you to spot any unusual patterns like frequent sales, family disputes, or properties that changed hands under suspicious circumstances.

One clear red-flag finding that should stop or pause a purchase is discovering that the property has an unresolved bond, a pending court case, or a deceased estate that has not been properly wound up.

You will find here the list of classic mistakes people make when buying a property in South Africa.

How do I confirm there are no liens in South Africa right now?

The standard way to confirm there are no liens or encumbrances on a property in South Africa is through your conveyancer, who will run a deeds search and obtain municipal and body corporate clearances before registration can proceed.

One common type of lien you should specifically ask about in South Africa is an existing mortgage bond registered over the property, which must be cancelled or settled by the seller before transfer, plus any municipal rates arrears or body corporate levy arrears that can block the transaction.

The best written proof of lien status is the combination of a clear deeds search showing no outstanding bonds and the municipal rates clearance certificate and body corporate clearance certificate that confirm all accounts are paid up.

How do I check zoning and permitted use in South Africa right now?

The authority you should use to check zoning and permitted use in South Africa is the local municipality where the property is located, and your conveyancer can request the zoning certificate and building plan approvals on your behalf.

The document that typically confirms the zoning classification is the municipal zoning certificate or town planning scheme map, which shows whether the property is zoned residential, commercial, mixed-use, or something else.

One common zoning pitfall that foreign buyers frequently miss in South Africa is buying a property that has unpermitted additions like a granny flat, extra rooms, or a converted garage that were never approved by the municipality, which can create legal and insurance problems down the line.

Buying real estate in South Africa can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Can I get a mortgage as a foreigner in South Africa, and on what terms?

Do banks lend to foreigners for homes in South Africa in 2026?

As of January 2026, major banks in South Africa do lend to foreigners and non-residents for home purchases, though they typically apply stricter terms than they would for local buyers.

The realistic loan-to-value range for foreign borrowers in South Africa is commonly around 50%, meaning you should expect to put down a deposit of at least half the property price, compared to the higher LTVs available to South African residents with local credit histories.

The single most common eligibility requirement that determines whether a foreigner qualifies is providing documented proof of foreign income and source of funds, along with completing the bank's enhanced FICA compliance process for non-residents.

You can also read our latest update about mortgage and interest rates in South Africa.

Which banks are most foreigner-friendly in South Africa in 2026?

As of January 2026, the three most foreigner-friendly banks for mortgages in South Africa are FNB (with their Foreign Choice product line), Standard Bank (with dedicated non-resident banking services), and Nedbank (which actively participates in the mortgage market and provides clear rate disclosures).

The single most important feature that makes these banks more foreigner-friendly is that they have dedicated product pages, application processes, and compliance teams specifically set up to handle non-resident buyers, rather than treating foreign applications as exceptions.

These banks will generally lend to non-residents who do not have local residency, though they require more documentation, typically offer lower LTVs around 50%, and may charge slightly higher rates than they would for resident borrowers.

We actually have a specific document about how to get a mortgage as a foreigner in our pack covering real estate in South Africa.

What mortgage rates are foreigners offered in South Africa in 2026?

As of January 2026, foreign buyers in South Africa can expect mortgage interest rates in the range of 10.25% to 12.25%, based on a prime rate of 10.25% and typical non-resident pricing of prime to prime plus 2%.

South African mortgages are predominantly variable-rate products linked to prime, so fixed-rate options are less common and may come at a premium when available; most foreign buyers end up with a variable rate that moves when the Reserve Bank adjusts the repo rate.

We made this infographic to show you how property prices in South Africa compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What will taxes, fees, and ongoing costs look like in South Africa?

What are the total closing costs as a percent in South Africa in 2026?

The typical total closing cost for buyers in South Africa in 2026 is around 4% to 6% of the purchase price for cash purchases, rising to 6% to 9% if you finance with a mortgage bond.

The realistic low-to-high closing cost range that covers most standard transactions in South Africa is 4% to 9%, depending on whether you need bond registration and the specific conveyancing firm you use.

The specific fee categories that make up total closing costs in South Africa include transfer duty (paid to SARS), conveyancing fees, Deeds Office registration fees, and if financed, bond registration costs and bank initiation fees.

The single fee category that is usually the biggest contributor to closing costs is transfer duty, which is a progressive tax that starts at 0% for properties under 1.1 million rand and increases in brackets as the purchase price rises.

If you want to go into more details, we also have a blog article detailing all the property taxes and fees in South Africa.

What annual property tax should I budget in South Africa in 2026?

As of January 2026, the typical annual property tax budget for a standard owner-occupied home in South Africa is roughly 0.6% to 1.2% of the municipal valuation per year, which for a property valued at 2 million rand works out to around 12,000 to 24,000 rand (approximately 650 to 1,300 USD or 600 to 1,200 EUR) annually.

Annual property tax in South Africa is assessed by the local municipality through a "rates in the rand" system, where the municipality applies a rate per rand of property value based on their own valuation roll, which means the exact amount varies significantly by city and even by neighborhood.

How is rental income taxed for foreigners in South Africa in 2026?

As of January 2026, non-resident owners in South Africa pay tax on their rental income at the standard South African individual tax rates (which are progressive and can reach up to 45% at the highest brackets), though most rental investors fall into lower effective brackets after deducting legitimate expenses like repairs, agent fees, rates, insurance, and bond interest.

The basic requirement for a foreign owner is to register with SARS, obtain a tax number, file annual income tax returns declaring the South African rental income, and pay any tax due; there is no automatic withholding on rental income, but you are responsible for voluntary compliance.

What insurance is common and how much in South Africa in 2026?

As of January 2026, a typical annual building insurance premium for a standard home in South Africa runs around 0.1% to 0.3% of the rebuild value, which for a property with a rebuild value of 2 million rand works out to roughly 2,000 to 6,000 rand per year (approximately 110 to 330 USD or 100 to 300 EUR).

The most common type of property insurance coverage that owners carry in South Africa is building insurance (also called homeowners insurance), which covers the structure against fire, storm damage, burst pipes, and other specified risks, and is mandatory if you have a mortgage bond.

The one biggest factor that makes insurance premiums higher or lower in South Africa is the property's location and crime risk profile, with homes in high-crime areas or areas prone to flooding and load-shedding-related damage typically paying significantly more than those in secure estates or lower-risk suburbs.

Get the full checklist for your due diligence in South Africa

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about South Africa, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why It's Authoritative | How We Used It |

|---|---|---|

| South African Revenue Service (SARS) - Transfer Duty | SARS is the official tax authority that sets and publishes transfer duty rates in South Africa. | We used it to pin down the exact transfer duty brackets that apply as of January 2026. We then used those brackets to build realistic closing cost estimates for foreign buyers. |

| SARS - Tax and Non-Residents | SARS provides the official explanation of how South Africa taxes residents versus non-residents. | We used it to explain what income a foreign owner is taxed on, especially rental income. We also used it to frame what "non-resident" means for ongoing tax compliance. |

| SARS - Non-Resident Seller Withholding Guide | This is SARS' official guide to the statutory withholding mechanism when non-residents sell property. | We used it to highlight the uniquely South African trap where the buyer may need to withhold tax when you sell. We explained how to avoid over-withholding by handling SARS paperwork early. |

| South African Reserve Bank - MPC Statement (Nov 2025) | SARB is the central bank and the primary source for the policy repo rate. | We used it to anchor the interest rate environment going into January 2026 at repo 6.75%. We then translated that into realistic mortgage rate expectations for foreign buyers. |

| SARB - Key Statistics (Repo and Prime) | SARB's key statistics page consolidates the official rate changes and effective dates. | We used it to confirm the repo at 6.75% and prime at 10.25% from late November 2025. We used those numbers as the baseline for prime plus or minus margin mortgage estimates. |

| Municipal Property Rates Act | This is the national legislation that enables municipal property rates in South Africa. | We used it to explain what annual property tax is in South Africa, which is municipal rates rather than a single national property tax. We used it to justify why the amount varies by municipality. |

| South African Government - Permanent Residence Overview | Gov.za summarizes official eligibility routes administered by Home Affairs. | We used it to show what actually drives permanent residence in South Africa, including work, business, retirement, and family ties. We used it to clearly state that owning a home is not a PR route. |

| Property Practitioners Act | This is the statute regulating estate agents and their consumer protection duties. | We used it to explain the regulated role of agents and why you should verify your agent is operating under the current legal framework. We used it to support the compliance guidance for foreigners. |

| Property Practitioners Regulatory Authority (PPRA) | PPRA is the regulator that replaced the old Estate Agency Affairs Board. | We used it to explain who regulates property practitioners and what the regulator does for consumer protection. We used it to justify verifying your agent's status as a risk-reduction step. |

| Deeds Registry - Property Transfer Process | Deeds registration is the legal record of ownership and explains the transfer logic. | We used it to describe how ownership becomes legally real in South Africa through registration in the Deeds Office. We used it to structure the step-by-step buying process in plain language. |

| Law Society of South Africa - Conveyancing Fee Guidelines | LSSA guidance is widely used to benchmark conveyancing charges and what they include. | We used it to estimate conveyancing costs and explain what conveyancers do, including clearances, deeds prep, and duty handling. We built realistic closing cost percentage ranges using this source. |

| Standard Bank - Non-Resident Banking | A major South African bank describing what it offers to non-residents. | We used it to support the point that banks may lend but typically not 100% LTV to foreigners. We used it as a cross-check against the interest rate baseline from SARB. |

| FNB - Foreign Choice Home Loan | A major South African bank page specifically aimed at non-residents and foreign nationals. | We used it to confirm that mainstream banks actively target the foreign buyer segment. We used it as another cross-check that the non-resident mortgage market is real, not theoretical. |

| Nedbank - Repo and Prime Explainer | A major bank publishing current repo and prime figures in consumer-friendly language. | We used it as a sanity check on the prime rate level at 10.25% after the November 2025 cut. We used it to keep the mortgage section easy to understand with prime as the base rate. |

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of South Africa. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.