Authored by the expert who managed and guided the team behind the South Africa Property Pack

Everything you need to know before buying real estate is included in our South Africa Property Pack

Pretoria is one of the more open property markets in Africa for foreign buyers, but there are still key rules around money flows, taxes, and practical paperwork you need to understand before signing anything.

This guide covers everything from what you can legally own, to mortgages, closing costs, and the exact steps to complete a purchase in Pretoria in January 2026.

We update this article regularly to reflect the latest tax rates, banking policies, and regulatory changes affecting foreigners buying property in the City of Tshwane.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Pretoria.

Insights

- Foreigners buying property in Pretoria typically face a maximum 50% loan-to-value ratio from South African banks, meaning you need to bring at least half the purchase price in cash.

- Transfer duty in Pretoria for a R2 million home works out to roughly R34,000 in January 2026, which is about 1.7% of the purchase price based on the latest SARS brackets.

- The biggest mistake foreign buyers make in Pretoria is not documenting how their purchase funds entered South Africa, which can delay or block repatriation of sale proceeds years later.

- Municipal property rates in Pretoria typically run between 0.5% and 1% of the City of Tshwane valuation per year, so a R2 million property might cost R10,000 to R20,000 annually in rates alone.

- South Africa does not offer a "golden visa" tied to property purchase, so buying a home in Pretoria will not automatically grant you residency or citizenship.

- Variable mortgage rates for foreigners in Pretoria in January 2026 typically range from 10% to 13%, based on the current repo rate of 6.75% and prime-linked lending.

- Many foreigners end up in sectional-title complexes in neighborhoods like Menlo Park, Hatfield, or Brooklyn, where body corporate rules can restrict short-term rentals and Airbnb-style letting.

- Total closing costs for a cash buyer in Pretoria typically run 3% to 5% of the purchase price, rising to 5% to 8% if you register a mortgage bond.

What can I legally buy and truly own as a foreigner in Pretoria?

What property types can foreigners legally buy in Pretoria right now?

South Africa is one of the more open markets in the region, and as a foreigner you can legally buy freehold houses, sectional-title apartments, townhouses, and vacant residential stands in Pretoria in your own name.

The most important practical condition is not about what you can own, but how you move money into the country, because banks and SARS require a clear paper trail if you ever want to take your sale proceeds back out.

If you buy a freehold property in Pretoria, you own both the land and the building outright, while sectional-title purchases mean you own your unit plus an undivided share in common property and must follow the body corporate rules on levies, conduct, and sometimes rental restrictions.

Security estates in areas like Silver Lakes or Mooikloof are legally either freehold or sectional title, but you also sign onto homeowners association rules that can govern everything from architecture to pets to short-term letting.

Finally, please note that our pack about the property market in Pretoria is specifically tailored to foreigners.

Can I own land in my own name in Pretoria right now?

Yes, if you buy a freehold property or a vacant residential stand in Pretoria, the land can be registered directly in your name at the Deeds Office just like any South African buyer.

This applies to essentially all standard residential land in areas like Brooklyn, Lynnwood, Faerie Glen, or Centurion, though certain agricultural holdings or land in traditional authority areas may have different rules that rarely affect typical residential buyers.

The real foreigner twist is not whether you can own, but making sure your purchase funds are properly documented when they enter South Africa so you can repatriate sale proceeds later without delays or extra approvals.

As of 2026, what other key foreign-ownership rules or limits should I know in Pretoria?

As of January 2026, the rules that most often affect foreign buyers in Pretoria relate to sectional-title and HOA restrictions on rentals, pets, renovations, and Airbnb-style letting, which are enforced at the complex or estate level rather than by national law.

South Africa does not impose a foreign-ownership quota for apartments or condos the way some Asian countries do, so there is no percentage cap limiting how many units in a building can be owned by foreigners.

The main reporting requirement is that your conveyancer and bank must document the source of your funds and the inward transfer for exchange-control purposes, which becomes crucial when you eventually sell and want to repatriate proceeds.

There is no major regulatory change around foreign ownership taking effect in 2026, though buyers should stay aware of any updates to exchange-control rules or municipal rates policies in the City of Tshwane.

What's the biggest ownership mistake foreigners make in Pretoria right now?

The single biggest mistake foreigners make when buying property in Pretoria is moving their purchase money incorrectly, either paying from mixed or unclear sources or failing to properly document the inward transfer with a South African bank.

If you make this mistake, you may discover at resale time that repatriating your sale proceeds is delayed for months or requires extra approvals from the South African Reserve Bank, which can be stressful and costly.

Other classic pitfalls in Pretoria include not checking body corporate or HOA rules before buying in a complex (and then discovering you cannot do short-term rentals), failing to verify municipal rates arrears, and not budgeting for the full closing costs including bond registration fees.

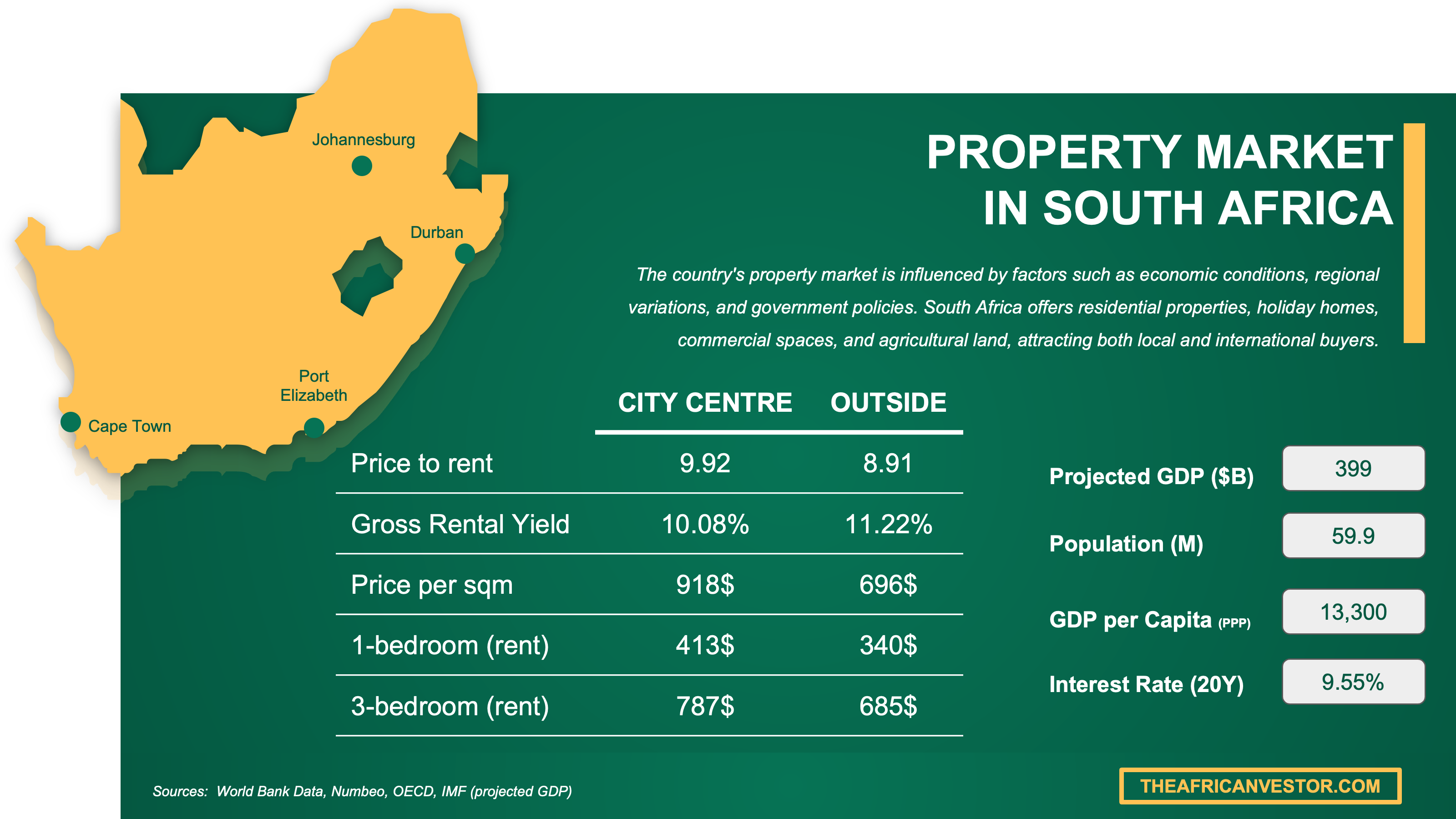

We have made this infographic to give you a quick and clear snapshot of the property market in South Africa. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which visa or residency status changes what I can do in Pretoria?

Do I need a specific visa to buy property in Pretoria right now?

You do not need a special "property-buyer visa" to purchase real estate in Pretoria, and yes, you can legally buy property while visiting on a tourist visa.

The most common administrative hurdle for buyers without local residency is opening a South African bank account and completing FICA/KYC requirements, which becomes easier if you have a longer-stay visa, a stable local address, and proper documentation.

You do not strictly need a South African tax ID (SARS income tax number) before signing an Offer to Purchase, but you should expect to obtain one if you will earn rental income or want smoother banking and compliance processes.

A typical document set for a foreign buyer in Pretoria includes a certified passport copy, proof of address (local or foreign), proof of funds or bank statements, and sometimes apostilled documents depending on where you sign.

Does buying property help me get residency and citizenship in Pretoria in 2026?

As of January 2026, buying property in Pretoria does not automatically grant you residency or citizenship because South Africa does not run a simple "buy a home, get a visa" scheme.

Property ownership can support your life setup and demonstrate ties to the country, but residency typically comes through other pathways such as work permits, business or investment visas, or retirement and financially independent person permits.

If you want permanent residency, the most common routes involve employment-based permits held for several years, proving you have a sustainable income source, or qualifying under the points-based skilled worker system rather than through real estate investment alone.

We give you all the details you need about the different pathways to get residency and citizenship in Pretoria here.

Can I legally rent out property on my visa in Pretoria right now?

Your visa status generally does not restrict your ability to rent out property you own in Pretoria, because owning and earning rental income are separate matters under South African law.

You do not need to live in South Africa to rent out your Pretoria property, and many foreign owners manage their investments from abroad using local letting agents.

The key things foreigners must know are that rental profit from Pretoria property is South African-source income (so SARS will expect you to register, file returns, and pay tax on net profit at marginal rates from 18% to 45%), and your body corporate or HOA rules may limit short-term or Airbnb-style letting in complexes.

We cover everything there is to know about buying and renting out in Pretoria here.

Get fresh and reliable information about the market in Pretoria

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

How does the buying process actually work step-by-step in Pretoria?

What are the exact steps to buy property in Pretoria right now?

The standard sequence to buy property in Pretoria goes like this: choose your property and confirm whether it is freehold or sectional title, make an Offer to Purchase with conditions, pay your deposit into a trust account while starting your bank paper trail, then the conveyancer opens the transfer file, runs due diligence, handles SARS transfer duty, and finally registers the property at the Deeds Office.

You often do not need to be physically present for every step because many signatures can be handled remotely through the conveyancer, though foreigners commonly need to be available for certified identity documents, apostilles, and bank onboarding if arranging local finance.

The deal typically becomes legally binding when the Offer to Purchase is signed by both parties and any suspensive conditions (like finance approval) are fulfilled or waived.

The end-to-end timeline from accepted offer to final Deeds Office registration in Pretoria usually ranges from 8 to 12 weeks for a straightforward transaction, though it can take longer if there are bond delays or complex sectional-title clearances.

We have a document entirely dedicated to the whole buying process our pack about properties in Pretoria.

Is it mandatory to get a lawyer or a notary to buy a property in Pretoria right now?

In practice, yes, you will use a conveyancing attorney (a specialist property lawyer) to buy property in Pretoria because South African property transfer is a legal process that must be lodged and registered through a conveyancer.

The key difference in South Africa is that the conveyancer handles the legal transfer and Deeds Office registration (similar to a notary's role in civil-law countries), while a separate attorney might advise you on contract terms or disputes, though many conveyancers also provide this advice as part of the transaction.

One important item to include in your conveyancer's scope is explicit handling of your exchange-control documentation, so that the paper trail for your inward funds is properly recorded and you can repatriate sale proceeds later without complications.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in South Africa versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What checks should I run so I don't buy a problem property in Pretoria?

How do I verify title and ownership history in Pretoria right now?

The official registry you should use to verify title and ownership history in Pretoria is the Deeds Office, and your conveyancer will run a deeds search to confirm who owns the property, the title description, and any registered bonds or interdicts.

The key document to request is a Deeds Office printout or title deed extract, which shows the registered owner, property description (erf number or sectional title unit), and any encumbrances currently registered against the property.

A realistic look-back period for ownership history checks in Pretoria is typically 10 to 20 years, which helps identify any unusual transfer patterns, family disputes, or historical issues that might affect your ownership.

One clear red flag that should stop or pause a purchase is discovering an unresolved interdict, a disputed ownership claim, or a mismatch between the title description and the physical property you inspected.

You will find here the list of classic mistakes people make when buying a property in Pretoria.

How do I confirm there are no liens in Pretoria right now?

The standard way to confirm there are no liens or encumbrances on a property in Pretoria is through a Deeds Office search, plus obtaining municipal rates clearance and (for sectional title) a body corporate clearance certificate from your conveyancer.

One common type of lien buyers should specifically ask about in Pretoria is a registered mortgage bond from the seller's bank, which must be cancelled before transfer, along with any municipal rates or levy arrears that could block the transaction.

The best form of written proof for lien status is a combination of the Deeds Office search showing no bonds or interdicts, a municipal clearance certificate from the City of Tshwane confirming rates are paid, and a body corporate clearance letter for sectional-title properties.

How do I check zoning and permitted use in Pretoria right now?

The authority to check zoning and permitted use for a property in Pretoria is the City of Tshwane, which maintains land-use schemes and can provide zoning certificates or extracts showing what is allowed on your property.

The single document that typically confirms zoning classification in Pretoria is a zoning certificate or municipal extract, which you can request through the City of Tshwane's planning department or through your conveyancer.

One common zoning pitfall foreign buyers miss in Pretoria is assuming they can add a second dwelling, run a home business, or do short-term rentals without checking whether the zoning and town-planning scheme actually permit it, plus whether the body corporate or HOA rules allow it on top of that.

Buying real estate in Pretoria can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Can I get a mortgage as a foreigner in Pretoria, and on what terms?

Do banks lend to foreigners for homes in Pretoria in 2026?

As of January 2026, yes, major South African banks do lend to foreigners for homes in Pretoria, though the terms depend heavily on whether you are a true non-resident or a foreign national living and working in South Africa.

The realistic loan-to-value range for foreign borrowers in Pretoria is typically up to 50% for bona fide non-residents (meaning you need to bring at least half the purchase price in cash), while foreign nationals with South African work permits and local income can often access 70% to 100% LTV depending on their credit profile.

The single most common eligibility requirement is whether you have South African residency and local income, because banks view non-residents as higher risk and typically cap their lending accordingly.

You can also read our latest update about mortgage and interest rates in South Africa.

Which banks are most foreigner-friendly in Pretoria in 2026?

As of January 2026, the three most foreigner-friendly banks for mortgages in Pretoria are FNB (with its dedicated "Foreign Choice" product), Standard Bank (which openly publishes non-resident banking and property funding guidance), and Nedbank (which has clear non-resident financing pathways).

The single most important feature that makes these banks foreigner-friendly is that they have established processes and dedicated product pages for non-residents, so you are not navigating a system designed only for locals.

These banks will lend to non-residents (buyers without local residency), but typically at a maximum of around 50% loan-to-value, with stricter documentation requirements and sometimes a premium on pricing.

We actually have a specific document about how to get a mortgage as a foreigner in our pack covering real estate in Pretoria.

What mortgage rates are foreigners offered in Pretoria in 2026?

As of January 2026, the typical mortgage interest rate range for foreigners in Pretoria is roughly 10% to 13% (variable), based on the current repo rate of 6.75% and the fact that most South African home loans are priced at prime or prime plus a margin.

Most mortgages offered to foreigners in Pretoria are variable-rate and linked to prime, with fixed-rate options being less common and typically more expensive when available, so you should expect your monthly payment to move with interest rate changes.

We made this infographic to show you how property prices in South Africa compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What will taxes, fees, and ongoing costs look like in Pretoria?

What are the total closing costs as a percent in Pretoria in 2026?

The typical total closing cost percentage for buying property in Pretoria in 2026 is around 3% to 5% of the purchase price for a cash buyer, and 5% to 8% if you also register a mortgage bond.

The realistic low-to-high range covers most standard transactions: simpler deals with no bond sit closer to 3%, while complex purchases with bond registration, higher transfer duties, and additional compliance costs can reach 8% or slightly more.

The specific fee categories that make up Pretoria closing costs include transfer duty (the buyer tax paid to SARS), conveyancing and Deeds Office fees, certificates and compliance costs, and (if applicable) bond registration and bank initiation fees.

Transfer duty is usually the biggest single contributor to closing costs in Pretoria, especially on properties above R1.6 million where the marginal rates start to bite.

If you want to go into more details, we also have a blog article detailing all the property taxes and fees in Pretoria.

What annual property tax should I budget in Pretoria in 2026?

As of January 2026, the typical annual property tax (municipal rates) budget for a standard owner-occupied home in Pretoria is roughly R10,000 to R20,000 per year (about $550 to $1,100 or EUR 500 to EUR 1,000) for a property with a municipal value around R2 million.

Municipal property rates in Pretoria are assessed by the City of Tshwane based on the municipal valuation roll (updated for the 2025 to 2029 period), with rates typically running between 0.5% and 1% of the assessed value per year before any rebates and excluding utilities like water and electricity.

How is rental income taxed for foreigners in Pretoria in 2026?

As of January 2026, the typical effective tax rate on foreigner rental income in Pretoria ranges from 18% to 31% for modest net profits, rising to 36% to 45% for higher rental income, because SARS taxes non-residents on South African-source income at the same marginal rates as residents.

The basic requirement is that foreign owners must register with SARS, file annual income tax returns, and pay tax on net rental profit (rent minus allowable expenses like levies, maintenance, and agent fees), with an additional note that a withholding mechanism under section 35A may apply when you eventually sell the property.

What insurance is common and how much in Pretoria in 2026?

As of January 2026, the typical annual insurance premium for a standard home policy in Pretoria ranges from R6,000 to R18,000 per year (about $330 to $1,000 or EUR 300 to EUR 900), depending on the rebuild value, security features, and claims history.

The most common type of property insurance coverage owners carry in Pretoria is buildings insurance (also called homeowners insurance), which covers the structure itself and is required by banks if you have a mortgage bond.

The biggest factor that usually makes insurance premiums higher or lower for the same property type in Pretoria is the security setup, because homes in security estates or with alarm systems, electric fencing, and armed response typically get better rates than properties with less protection.

Get the full checklist for your due diligence in Pretoria

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Pretoria, we always rely on the strongest methodology we can, and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why It's Authoritative | How We Used It |

|---|---|---|

| SARS Transfer Duty | SARS is the official tax authority that sets legally binding transfer duty brackets. | We used it to get the exact 2026 transfer duty thresholds and marginal rates. We then calculated realistic closing costs for typical Pretoria purchases. |

| SARS Rate Update Notice | It's SARS' own announcement confirming when the updated brackets started applying. | We used it to anchor the January 2026 timing and confirm the effective date. We cross-checked it against the main transfer duty page for consistency. |

| SARS Non-Resident Tax | It's the official SARS guidance on what non-residents are taxed on in South Africa. | We used it to explain that non-residents are taxed on South African-source income, including rental income from Pretoria property. We framed what "non-resident" means for South African tax purposes. |

| SARS Individual Tax Rates | This is the official SARS table of marginal personal income tax rates. | We used it to describe how rental profit is taxed at marginal rates. We gave a confident range for what foreign owners might pay depending on taxable income. |

| SARS Withholding Guide | It's SARS' official guide to section 35A withholding on sales by non-residents. | We used it to flag a common surprise for foreign owners when selling. We included it as a risk item affecting exit planning. |

| SARB MPC Statement | It reproduces SARB's official communication setting the policy rate. | We used it to anchor the interest rate environment as of late 2025 with repo at 6.75%. We translated that into typical variable mortgage pricing for foreigners. |

| City of Tshwane Valuation Roll | It's the local government authority for Pretoria that levies municipal property rates. | We used it to explain how Tshwane sets your rates bill based on the valuation roll. We highlighted that valuation updates can materially change monthly costs. |

| City of Tshwane Land-Use Portal | It's the municipality's own portal for zoning and land-use management documents. | We used it to direct buyers to where they check zoning and permitted use. We turned that into a buyer-friendly zoning checklist. |

| Standard Bank Non-Residents | Standard Bank is one of South Africa's major banks with published non-resident product rules. | We used it to confirm that non-residents commonly face a 50% funding limit. We showed the typical documentation banks ask for. |

| FNB Foreign Choice | FNB is a major South African bank with a dedicated non-resident product. | We used it to prove that mainstream banks explicitly cater to foreigners. We treated it as product evidence for our foreigner-friendly banks section. |

| ooba Foreign Buyer Guide | ooba is a large, established South African home loan comparison platform. | We used it to translate bank practice into buyer-friendly rules of thumb. We cross-checked those rules against big-bank pages for accuracy. |

| Bissets Attorneys Guide | It's a specialist South African law firm publishing structured guidance grounded in legal practice. | We used it for practical legal-process details foreigners often miss, especially exchange-control paperwork. We validated key points using bank pages and SARS. |

| OUTsurance Building Calculator | It's a major insurer providing a transparent rebuild-cost estimation method. | We used it to explain that insurance should be based on rebuild cost, not market price. We built a reasonable insurance budget range for Pretoria homes. |

| Nedbank Non-Resident Banking | Nedbank is a major South African bank with published non-resident financing guidance. | We used it to confirm non-resident lending options and typical LTV limits. We included it in our foreigner-friendly banks shortlist. |

| Absa Homeowners Insurance | Absa is a major bank-insurer showing typical coverage requirements for mortgaged properties. | We used it to confirm that banks require buildings insurance from registration onward. We incorporated this into our ongoing costs guidance. |

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of South Africa. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

Related blog posts